From technical infrastructure to financial product

Until recently, energy storage was seen as a “necessary cost” for critical industries or a technical complement to photovoltaics. That view is outdated. Today, a Battery Energy Storage System (BESS) is first and foremost a financial asset.

For an institutional investor, an infrastructure fund or a CFO, a BESS is a “black box” in which capital (CAPEX) is invested and which, properly managed, returns predictable free cash flows with an attractive Internal Rate of Return (IRR), often higher than that of traditional assets.

The new energy real estate

The analogy is clear. Just as one invests in real estate to obtain rents, one invests in a BESS to obtain “energy rents”. The difference is that while real estate is based on location, the BESS is based on market volatility and manageability. As we discussed in our article on the market situation in Spainthe current extreme price environment is the perfect breeding ground for this asset class.

Financial anatomy of a BESS project: Costs

To structure the investment, we must first dissect the costs. A common mistake is to look only at the price of the battery module.

CAPEX (Initial Investment): Beyond lithium

The cost of the battery container is the main item (about 50-60%), and its price has dropped dramatically thanks to the LFP technology that we detail in our technical guide for installers. However, the sophisticated inverter looks at the Balance of System (BOS): inverters (PCS), transformers, civil works, engineering, permits and grid connection. A well-optimized CAPEX in the engineering phase is the first step towards profitability.

OPEX (Operating Costs): The importance of maintenance and escalation

OPEX is not just insurance and monitoring. There are two critical costs to model over 15-20 years:

-

Cost of energy to charge: The “raw material” we buy.

-

Augmentation: Batteries degrade with use. To maintain revenue capacity over the years, it is necessary to plan for future capital injections to replace or add new battery modules (augmentation) in year 5, 8 or 10. To ignore this is to artificially inflate the initial IRR.

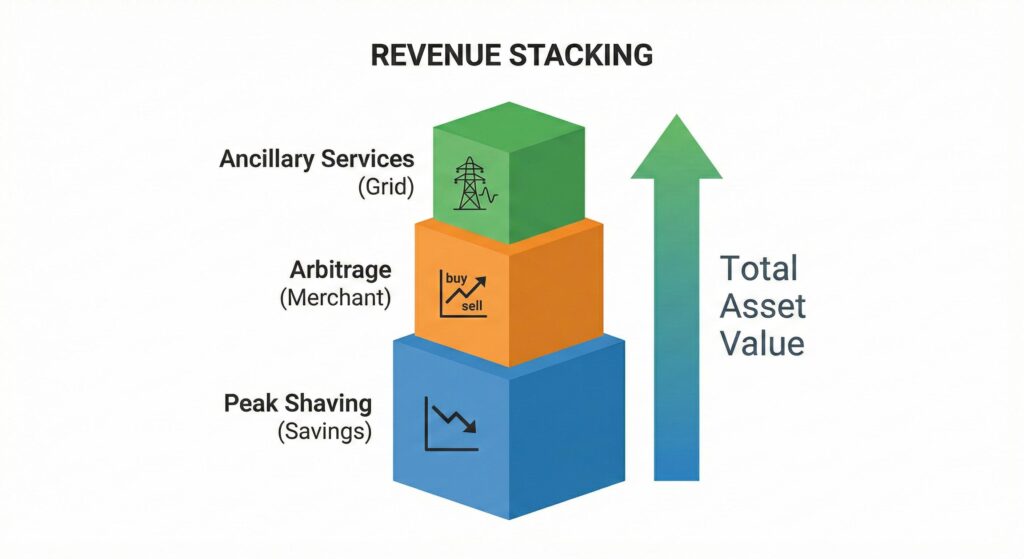

The Profitability Driver: Revenue Stacking

Herein lies the financial magic of the BESS. Unlike a solar plant that has only one revenue stream (selling energy when the sun is shining), a BESS is a “multi-tasking” asset. The key to profitability is Revenue Stacking: the ability to participate in multiple markets simultaneously to maximize total revenue.

1. Merchant Income: Volatility as an ally

It is the pure and simple sale and purchase of energy. Buy at off-peak hours, sell at peak hours. As we saw in the article on advanced arbitrage strategiesthis requires sophisticated algorithms and a powerful EMS. The higher the volatility of the daily and intraday market, the higher the gross margins on this item.

2. Adjustment and Network Services: Regulated and Stable Revenues

The System Operator (Grid) pays whoever helps to maintain grid stability (frequency at 50Hz). BESS are perfect for this because of their speed of response (milliseconds). Participating in Primary, Secondary or Tertiary Reserve markets offers more stable and predictable income than pure arbitrage, acting as a fixed income “bond” within the asset’s portfolio.

3. Avoided Costs and Capacity: Savings as Revenue

For an industrial investor (C&I), “a euro saved is a euro earned”.

-

Peak Shaving: Reducing the contracted power and avoiding penalties due to maximum meter generates an immediate positive cash flow.

-

Capacity Payments: Spain is expected to develop capacity markets where BESS are paid simply for being “available” to cover peak demand, adding another layer of fixed revenues.

Key Performance Indicators (KPIs) for the storage investor

When modeling the project in a spreadsheet, these are the ratios that decide whether the investment goes ahead:

IRR, NPV and Payback: Measuring Success

-

IRR (Internal Rate of Return): Currently, well-structured BESS projects in Spain are looking for double-digit leveraged IRRs (between 10% and 15%, depending on the merchant vs. regulated risk profile).

-

Payback (simple return): As we mentioned when analyzing the benefits for companies benefits for companiesThe payback periods are often between 5 and 7 years, which can be accelerated by the sale of CAEs.

LCOS (Levelized Cost of Storage): The actual cost of the cycle.

LCOS calculates how much it costs to store and discharge 1 MWh over the lifetime of the project, including CAPEX, OPEX, degradation and financial costs. It is the fundamental metric for comparing different battery technologies or suppliers. If your LCOS is lower than the average market price differential, the project is viable.

In short, structuring an investment in BESS requires a hybrid approach: the technical precision of engineering and the strategic vision of corporate finance. It is not about buying batteries, but about acquiring a “financial option” on the volatility of the electricity market.

We know that bankability and risk are the investor’s main concerns. Below, we address the most common doubts in investment committees.

Frequently asked questions about the bankability of BESS projects

Can these projects be financed by traditional banks (Project Finance)? Yes, increasingly so. Although banks are conservative with merchant risk (pure arbitrage), the combination with more stable income (adjustment services or peak shaving savings) allows structuring senior debt for a significant portion of CAPEX, improving the equity IRR.

How do you mitigate the risk of energy prices stabilizing? This is the main risk of the merchant model. It is mitigated by Revenue Stacking (not relying only on arbitrage) and, in some cases, by signing bilateral PPAs (power purchase agreements) with companies seeking stable supply, setting a floor price for part of the battery capacity.

What role does software (EMS) play in asset valuation? Critical. A BESS without an advanced EMS, such as the one described in our article on real-time managementis a “dumb” asset unable to capture market opportunities, which drastically reduces its projected cash flows and ultimate valuation.

Is there a secondary market for these assets? It is emerging. As the first projects mature and demonstrate their profitability, we are seeing interest from pension funds and insurers in acquiring portfolios of operational BESS assets that offer stable long-term returns.